Don’t Let a Quiet Start Fool You – Hurricane Season is Far from Over

Don’t Let a Quiet Start Fool You – Hurricane Season is Far from Over

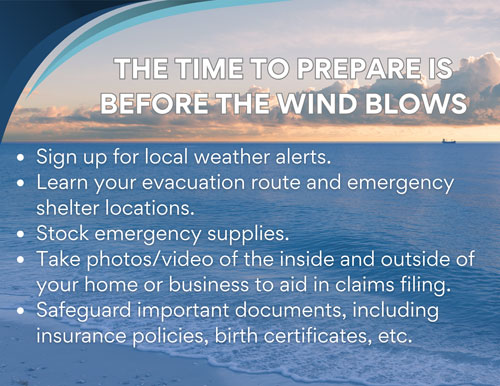

While the 2025 hurricane season may have started off quietly, now is not the time to let your guard down. As we move into August—the heart of hurricane season—it’s critical to ensure your hurricane preparedness plan is in place.

According to the National Oceanic and Atmospheric Administration (NOAA), there is a 70% likelihood that this season will bring above-normal activity in the Atlantic basin. Their forecast includes:

- 13 to 19 named storms

- 6 to 10 hurricanes

- 3 to 5 major hurricanes (Category 3, 4, or 5)

Even one storm can have significant impacts. Take time now to review your emergency plan, check your insurance coverage, and stay informed. Preparedness today can make all the difference tomorrow.

Stay Informed This Hurricane Season

Below are links to our social media accounts, where we’ll post updates as storms approach, along with helpful resources from local news outlets and other trusted sources to help you stay prepared. By clicking on the links below, you will be leaving our website. Heidrick & Company Insurance, and its affiliated companies, take no responsibility for the content or information contained on those other sites and do not have edit rights or any control over the sites.

Heidrick & Co. Social Media

![]() https://www.facebook.com/SanibelInsurance

https://www.facebook.com/SanibelInsurance

![]() https://www.instagram.com/heidrickco.insurance/

https://www.instagram.com/heidrickco.insurance/

News & Municipal Links

![]() https://www.floridadisaster.org/planprepare

https://www.floridadisaster.org/planprepare

![]() State of FL Hurricane Preparedness Guide

State of FL Hurricane Preparedness Guide

![]() https://www.gulfcoastnewsnow.com/hurricanes

https://www.gulfcoastnewsnow.com/hurricanes

![]() https://www.fox4now.com/weather/hurricane-center

https://www.fox4now.com/weather/hurricane-center

![]() https://www.ready.gov/hurricanes

https://www.ready.gov/hurricanes

![]() https://www.leegov.com/hurricane

https://www.leegov.com/hurricane

![]() https://www.mysanibel.com/CivicAlerts.aspx?AID=71

https://www.mysanibel.com/CivicAlerts.aspx?AID=71

![]() https://www.scgov.net/government/emergency-services/hurricane-preparedness-6291

https://www.scgov.net/government/emergency-services/hurricane-preparedness-6291